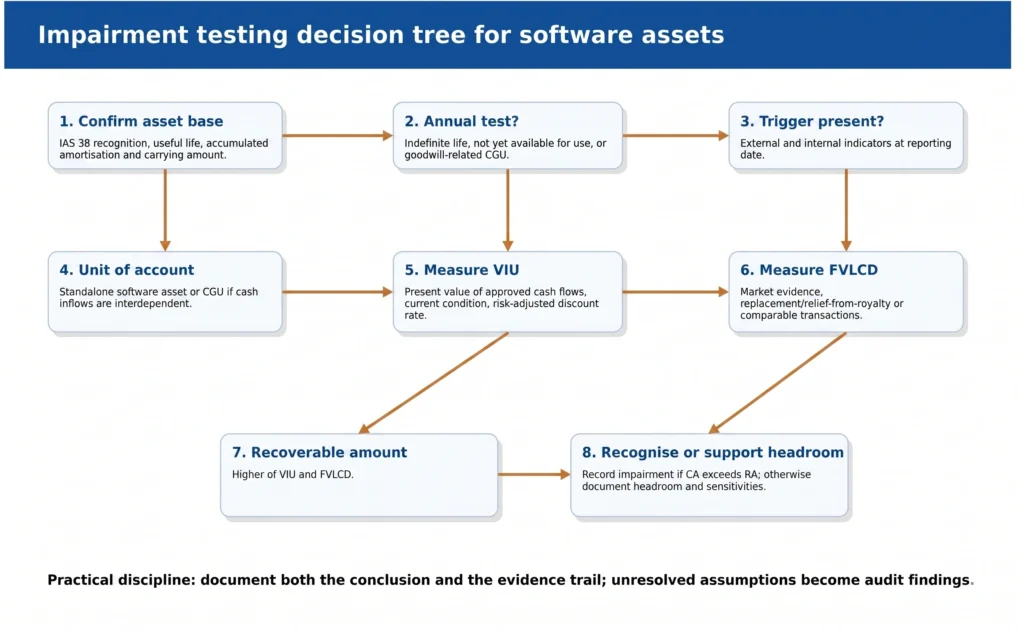

1. Purpose and technical positioning

This publication sets out a practical, audit-defensible approach for impairment testing of software intangible assets under IFRS. It is designed for CFOs, controllers, valuation specialists, audit committees and transaction teams dealing with internally developed platforms, acquired software, licensed systems and capitalized development costs.

The emphasis is on software because the most difficult impairment questions usually arise where the asset is commercially valuable, operationally embedded and difficult to sell as a standalone item. The key judgement is therefore whether the asset is tested individually or within a cash-generating unit (CGU).

- Start with the carrying amount and IAS 38 capitalization basis before building any valuation model.

- Separate evidence of technical capability from evidence of commercial recoverability.

- Ensure the impairment model reconciles to the trial balance, the asset register and the financial statements.

2. IAS 38 gate: what exactly is being tested?

A software balance is not automatically a valid impairment-testing population. Management should first confirm that the asset meets the intangible asset recognition criteria, that only eligible development costs have been capitalized, and that the asset is available for use or still under development.

| Area | Publication-grade conclusion expected |

|---|---|

| Nature of asset | Identify whether the item is internally generated software, acquired software, perpetual licence, implementation configuration, cloud customization or a bundled arrangement. |

| Recognition | Confirm identifiability, control and expected future economic benefits. Research costs and unsuccessful feasibility work should not be in the asset base. |

| Measurement | Tie additions to invoices, payroll capitalization schedules, timesheets, project approvals and directly attributable cost logic. |

| Useful life | Support the useful life with product roadmap, expected customer use, technical obsolescence, regulatory requirements and commercial strategy. |

| Availability date | Evidence the date from which amortisation starts: production deployment, go-live certificate, board approval, UAT sign-off or release notes. |

3. When to perform an impairment test

The first screen is whether the asset requires an annual impairment test. Software not yet available for use must be tested annually even if management believes there is no impairment. For finite-life software available for use, an impairment test is required when indicators exist.

Indicators should be evaluated at every reporting date. In practice, software impairment triggers often arise before they are reflected in accounting numbers because operational signals appear earlier than financial underperformance.

| External indicators | Internal indicators |

|---|---|

| Adverse regulatory change, licensing delay, market contraction or a significant increase in market discount rates. | Budget misses, abandoned functionality, product delays, failed launch, reduced user adoption or management decision to pivot. |

| Comparable market prices, vendor replacement costs or transaction evidence below carrying value. | Higher maintenance cost, unresolved bugs, cybersecurity limitations, integration failure or loss of key engineering team. |

| New competing technology or platform obsolescence that shortens expected economic life. | Evidence that the asset will be retired, replaced, sold, mothballed or used differently from the original plan. |

4. Unit of account: software asset or CGU

The recoverable amount is determined for an individual asset only if that asset generates cash inflows that are largely independent from other assets.

Many fintech, capital-markets and enterprise software assets do not meet that threshold because they support origination, onboarding, processing, servicing, collections, reporting or advisory services as part of a wider operating model.

If independent cash inflows cannot be determined, the asset is tested within the smallest CGU that includes the software and generates largely independent inflows.

The CGU boundary must be consistent with Internal management reporting, Budgeting, Revenue ownership and how management monitors performance.

- A loan-origination engine may be part of a consumer-finance CGU if revenue arises from the full lending platform.

- A licensed wealth-management platform may be tested separately if it has contractual licence revenue.

- A back-office implementation may require CGU testing because it supports the business but does not generate standalone cash inflows.

5. Measurement: recoverable amount

The recoverable amount is the higher of value in use (VIU) and fair value less costs of disposal (FVLCD). Management should calculate both when both can be estimated reliably, particularly when the audit risk is high or the headroom is narrow.

| Measurement basis | Perspective | Typical software evidence |

|---|---|---|

| Value in use | Entity-specific use of the asset in its current condition. | Board-approved forecasts, user volumes, transaction revenue, licence income, maintenance cash flows, cost-to-complete and working capital impacts. |

| FVLCD | Market-participant exit price less incremental disposal costs. | Comparable software transactions, vendor quotes, replacement-cost benchmarks, relief-from-royalty support, external valuation indications and disposal cost estimates. |

| Recoverable amount | Higher of VIU and FVLCD. | If the higher amount exceeds carrying value, no impairment is recorded; if it is lower, the excess carrying amount is impaired. |

6. Building a controlled VIU model

A VIU model should use cash flows from continuing use of the software in its current condition. Forecasts should be reasonable, supportable and linked to budgets approved by management or the board. Enhancements that materially improve the asset beyond current condition should not be included unless they are already committed and necessary to maintain existing service potential.

- Forecast period: Normally use a period supported by detailed budgets and business plans. Beyond that, use a long-term growth assumption consistent with the market and asset economics.

- Discount rate: Use a pre-tax rate reflecting current market assessments of time value of money and risks specific to the asset or CGU. Avoid double-counting risks already reflected in cash flows.

- Terminal value: Ensure the terminal growth rate does not exceed the long-term growth rate of the market in which the asset or CGU operates unless strongly evidenced.

- Consistency: Cash flows, discount rate, inflation, tax assumptions and currency must be internally consistent.

| VIU input | Control question |

|---|---|

| Revenue / usage | Does the forecast reconcile to contracts, pipeline, churn, user activity or board-approved commercial plan? |

| Cost base | Are maintenance, hosting, support, cybersecurity and product-team costs included at a sustainable level? |

| Capital expenditure | Is spending limited to maintenance or committed completion work rather than expansionary enhancements? |

| Discount rate | Is the rate aligned with currency, risk and cash-flow basis? Is it pre-tax where required? |

| Terminal value | Is terminal growth supportable and lower than or consistent with market growth expectations? |

7. FVLCD for software: evidence hierarchy

FVLCD is market-participant oriented. For software, market evidence is often imperfect because functionality, jurisdiction, regulatory permissions, implementation status, source-code transferability and customer base differ materially between products. The valuation file should therefore explain why the evidence is comparable or how differences were adjusted.

| Evidence type | Audit strength | Typical adjustments |

|---|---|---|

| Signed third-party offer / LOI | High, if recent, credible and specific to the asset. | Adjust for conditionality, exclusivity, expected disposal costs and any bundled maintenance terms. |

| Comparable transaction | Medium to high. | Adjust for scale, functionality, geography, maturity, IP ownership and implementation status. |

| Vendor replacement quote | Medium. | Adjust for make-versus-buy, implementation cost, data migration, training and customization. |

| Income approach / relief-from-royalty | Medium. | Support royalty rate, revenue base, obsolescence, tax and discount-rate assumptions. |

| Management estimate only | Low. | Use only with corroboration, sensitivity analysis and governance sign-off. |

8. Worked numerical examples

All amounts in the examples are illustrative and shown in SAR million unless otherwise stated. The examples are simplified to demonstrate the accounting mechanics. Live models should include detailed monthly cash flows, supporting schedules and audit trails.

Example 1: origination platform with positive headroom

Facts : A regulated finance company capitalized an internally developed origination and decisioning platform. The asset is available for use, has a finite useful life and generates identifiable incremental cash flows through loan origination fees and servicing efficiencies.

| Item | Amount |

|---|---|

| Gross cost | 15.0 |

| Accumulated amortisation | (2.2) |

| Carrying amount | 12.8 |

| VIU from approved forecast | 14.5 |

| FVLCD from market evidence | 13.9 |

| Recoverable amount | 14.5 |

| Headroom | 1.7 |

| Impairment loss | Nil |

Conclusion: No impairment is recorded because the recoverable amount of SAR 14.5m exceeds the carrying amount of SAR 12.8m.

The audit file should still include sensitivity analysis because the model depends on Origination volume, Approval rate, Collection performance and Discount rate.

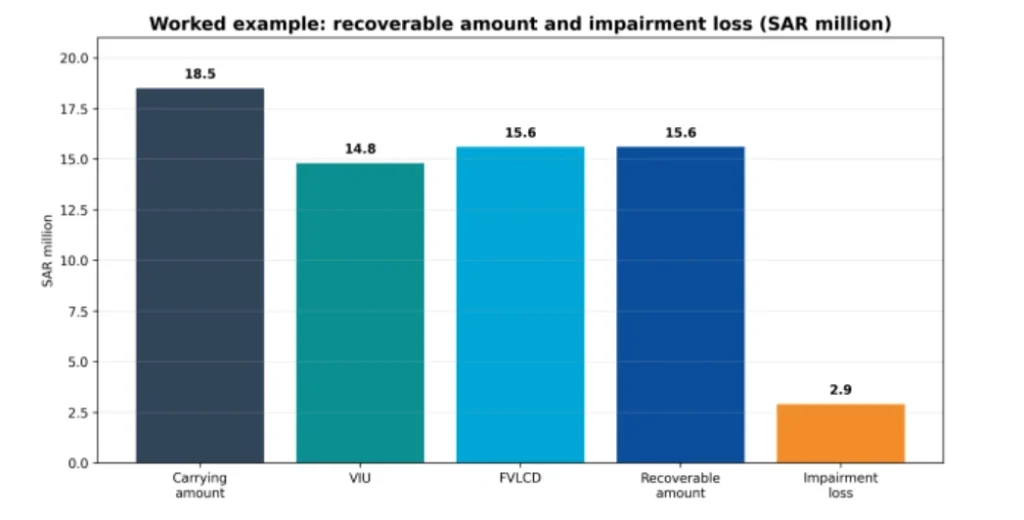

Example 2: wealth-management platform with impairment

Facts: A wealth-management software platform has a carrying amount of SAR 18.5m. The updated commercial plan reflects slower AUM growth and delayed monetisation. VIU is SAR 14.8m. A recent market-participant indication supports FVLCD of SAR 15.6m after disposal costs.

| Computation | SAR m |

|---|---|

| Carrying amount | 18.5 |

| Value in use | 14.8 |

| Fair value less costs of disposal | 15.6 |

| Recoverable amount: higher of VIU and FVLCD | 15.6 |

| Impairment loss: 18.5 - 15.6 | 2.9 |

Journal entry: Dr impairment loss SAR 2.9m; Cr software intangible asset or accumulated impairment SAR 2.9m. The revised carrying amount becomes SAR 15.6m and future amortisation is recalculated prospectively over the remaining useful life.

Example 3: CGU impairment allocation

Facts: A customer-facing application is not capable of generating standalone cash inflows. It is tested as part of a digital finance CGU. The CGU carrying amount and recoverable amount are as follows:

| CGU asset | Carrying amount | Allocation basis |

|---|---|---|

| Software intangible | 18.0 | Primary impaired asset |

| Right-of-use asset | 7.0 | Operational premises |

| Property and equipment | 4.0 | Supporting infrastructure |

| Working capital included in CGU | 3.0 | Operating assets |

| Total CGU carrying amount | 32.0 | |

| Recoverable amount | 27.5 | |

| Impairment loss | 4.5 |

The impairment loss is allocated to assets in the CGU in accordance with the applicable impairment allocation rules, while ensuring no asset is reduced below the highest of its individual FVLCD, its VIU where determinable, and zero. The allocation should be supported by a schedule that clearly shows pre-impairment carrying value, allocation percentage, impairment charge and revised carrying amount.

Example 4: software not yet available for use

Facts: A wealth analytics platform is still under development at yearend. Capitalized development cost is SAR 9.2m. Management expects commercial launch in Q3 of the next year. Because the asset is not yet available for use, it is tested annually even if no trigger is identified.

| Measurement | SAR m |

|---|---|

| Capitalized cost to date | 9.2 |

| Estimated remaining development cost | 1.4 |

| VIU based on current condition and committed completion | 10.3 |

| FVLCD based on market participant evidence | 8.6 |

| Recoverable amount | 10.3 |

| Impairment loss | Nil |

The conclusion is not automatic: management must support the expected launch date, completion budget, resource plan, regulatory

dependencies, technical feasibility and the rationale for including committed completion spend in the recoverability analysis.

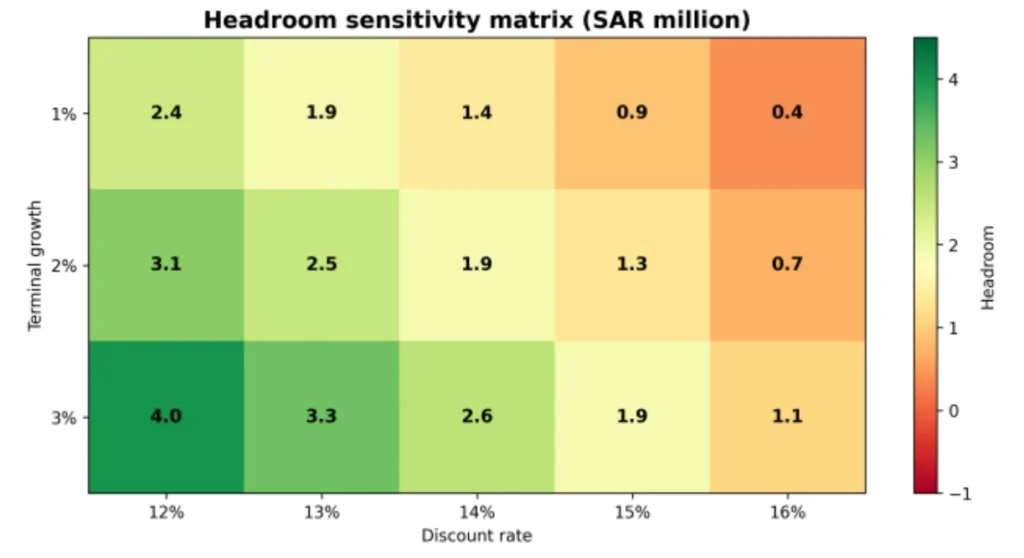

Example 5: sensitivity and break-even analysis

Facts: VIU is based on five years of forecast cash flows of SAR 1.3m, 1.5m, 1.7m, 1.9m and 2.1m, plus terminal value. The base discount rate is 13% and terminal growth is 2%. Headroom is SAR 2.5m in the base case.

| Stress factor | Base case | Downside case | Interpretation |

|---|---|---|---|

| Discount rate | 13.0% | 15.0% | Tests capital-market and execution risk. |

| Terminal growth | 2.0% | 1.0% | Tests maturity and long-term market assumptions. |

| Revenue haircut | 0% | (10%) | Tests lower adoption and slower monetisation. |

| Headroom | 2.5 | 0.6 | Still positive, but audit focus should be on revenue support and discount rate. |

9. Accounting entries and presentation

An impairment loss is recognized when carrying amount exceeds recoverable amount. The accounting entry should be supported by the final impairment schedule, clearly showing asset identifier, cost, accumulated amortisation, accumulated impairment and revised carrying amount.

| Scenario | Debit | Credit | Financial statement effect |

|---|---|---|---|

| Impairment recorded | Impairment loss - P&L | Accumulated impairment on software intangible asset | Reduces profit and asset carrying amount. |

| No impairment | No entry | No entry | Disclose significant judgements only if material to the financial statements. |

| Reversal for non-goodwill asset | Software intangible asset / accumulated impairment | Reversal of impairment gain - P&L | Revised carrying amount cannot exceed depreciated/amortised amount that would have existed without impairment. |

After impairment, amortisation is recalculated prospectively over the remaining useful life. If the useful life or residual value has changed, the change is treated as a change in accounting estimate, not as a prior-period error unless the previous accounting was demonstrably incorrect.

10. Disclosures and governance

The financial statements should provide enough information for users to understand the impairment charge, the events that led to it, the asset or CGU affected, the measurement basis used and the key assumptions when required. For material software balances,

disclosure quality should not be treated as a year-end drafting exercise; it should be built from the impairment file.

• Describe the asset or CGU and why impairment was or was not identified.

• Explain whether recoverable amount was determined using VIU, FVLCD or both.

• Disclose key assumptions when material, including growth, discount rate and forecast horizon.

• Cross-check disclosure numbers to the model, journal entry, fixed asset register and trial balance.

11. Reversal of impairment

For assets other than goodwill, an impairment loss may be reversed when there has been a change in estimates used to determine recoverable amount since the last impairment was recognized. A reversal is not a free revaluation: the increased carrying amount cannot exceed the carrying amount that would have been determined, net of amortisation, had no impairment been recognized in prior periods.

| Reversal evidence | Examples for software |

|---|---|

| External evidence | Signed third-party licence agreement, improved market pricing, removal of regulatory restriction or credible sale offer. |

| Internal evidence | Successful deployment, new committed customer contracts, proven usage, cost reductions or approved strategic relaunch. |

| Controls | Board approval, revised model, linkage to revised useful life and documented cap on reversal amount. |

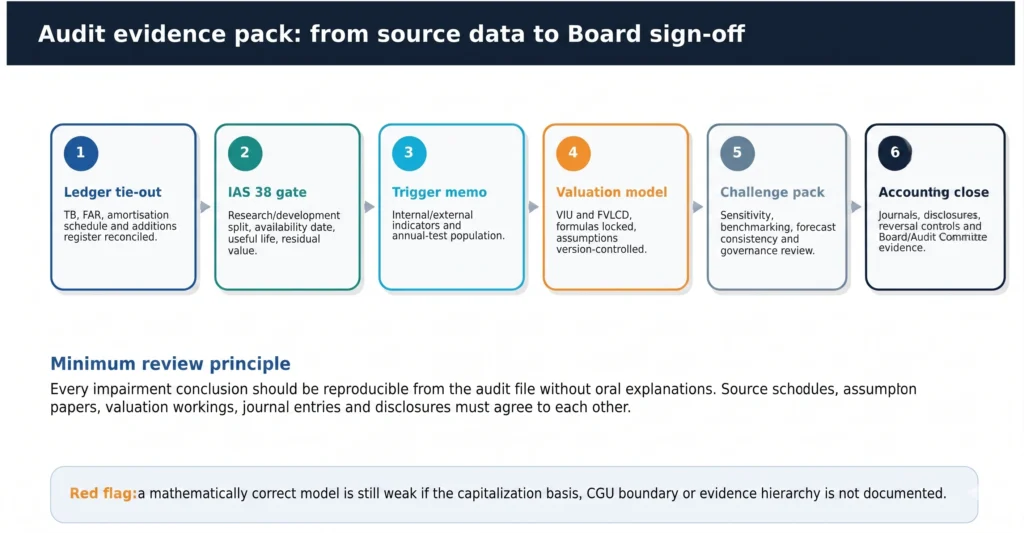

12. Model governance and audit file

A valuation workbook is only one component of the impairment conclusion. For a high-quality audit file, management should maintain a controlled evidence pack that allows an independent reviewer to understand the conclusion without reconstructing the model from scratch.

| Required schedule | Purpose |

|---|---|

| Asset register reconciliation | Proves completeness and accuracy of carrying values. |

| Capitalization memo | Explains IAS 38 recognition, development phase and cost eligibility. |

| Trigger assessment memo | Documents external and internal indicators at the reporting date. |

| CGU boundary paper | Supports standalone versus CGU-level testing. |

| VIU model | Documents cash flows, discount rate, terminal value and sensitivities. |

| FVLCD support | Documents market evidence, adjustments, disposal costs and reliability hierarchy. |

| Journal and disclosure tie-out | Ensures accounting entries and notes agree to the final model. |

13. Common audit findings and how to avoid them

| Finding | Why it matters | Clean response |

|---|---|---|

| Asset base does not reconcile to FAR/TB | Valuation may test the wrong number. | Include a signed reconciliation from trial balance to asset register to model input. |

| CGU boundary unsupported | Recoverable amount may be measured at the wrong level. | Tie CGU to independent cash inflows, internal reporting and management monitoring. |

| Forecasts exceed approved budgets | Cash flows may not be reasonable and supportable. | Use approved budgets or reconcile deltas with evidence and governance approval. |

| Discount rate inconsistent with cash flows | Risks may be double counted or omitted. | Align rate with currency, nominal/real basis, tax basis and risk adjustments. |

| FVLCD based on stale or non-comparable evidence | Market evidence may not represent measurement-date assumptions. | Update evidence to reporting date and document comparability adjustments. |

| No sensitivity analysis | Users cannot understand estimation uncertainty. | Include reasonably possible changes and break-even analysis. |

14. Technical basis and source references

This publication is based on IFRS principles applicable to impairment of assets and intangible assets. It is intended as practical guidance and does not override the requirements of applicable accounting standards, laws, regulations or auditor judgement.

| Source | Area used in this guide |

|---|---|

| IFRS Foundation - IAS 36 Impairment of Assets | Recoverable amount, VIU, FVLCD, annual testing for certain intangible assets, impairment recognition and reversal concepts. |

| IFRS Foundation - IAS 38 Intangible Assets | Definition of intangible asset, software as an intangible asset, recognition and measurement principles for internally generated software. |

| IFRS Foundation - IFRS 13 Fair Value Measurement | Market-participant perspective and fair value measurement concepts relevant when developing FVLCD evidence. |

| Strategy&Consult professional judgement and illustrative modelling examples | Worked numerical examples, governance framework, audit file structure and software-specific practical controls. |

Publication note: figures and calculations are illustrative and should be adapted to the facts, reporting date, local regulatory environment,

currency, tax basis and audit evidence available to the reporting entity.

15. Audit Committee challenge questions

The following questions help convert the technical model into governance-grade oversight:

• What is the single most sensitive assumption and what independent evidence supports it?

• Is the asset being tested at the correct level: individual asset or CGU?

• Does the model reconcile to approved budgets, not informal commercial aspirations?

• Are there any post-reporting-date events that confirm or contradict the year-end conclusion?

• Would the same conclusion be reached if the auditor used a marketparticipant lens rather than a management-use lens?

Strategy&Consult closing view

A credible impairment conclusion for software must do three things simultaneously: define the asset correctly, measure recoverable amount using supportable evidence, and make the audit trail transparent. Weakness in any one of these pillars can undermine the accounting conclusion even when the valuation arithmetic is technically correct.